If you’re tempted by those “buy now, pay later(BNPL)” offers popping up everywhere, here’s the truth. BNPL can be a good deal for disciplined shoppers, but it becomes an expensive trap for millions of Aussies who miss payments.

In this guide, we’ll break down “buy now, pay later” services so you’ll know exactly if BNPL is right for your wallet.

We’ll cover:

- How BNPL works behind the scenes

- The costs of late fees and credit impacts

- Top providers offering the best deals

- Effective strategies to avoid financial traps

- Best timing for BNPL vs other payment methods

Drawing from our experience helping Aussie deal-hunters make better money choices, we’ve seen both the benefits and risks of these services firsthand.

Ready to learn more? Let’s get started.

What Is Buy Now Pay Later?

Buy now, pay later is a payment method that splits your purchase into smaller instalments, usually four payments over six to eight weeks. Think of it as retail’s answer to “have your cake and eat it too.” These services let you take home your purchase immediately while spreading the cost across future pay periods.

Let’s break down exactly what you’re signing up for.

- The Split Payment System: Payment plans split any purchase into four instalments, usually paid over six weeks. The first payment happens immediately at checkout, then three more follow automatically. This means your later service provider handles all the scheduling and bank account deductions.

- Top Later Providers in Australia: Afterpay leads the pack, followed by Zip Pay, Klarna, and other later service options. Each provider targets different shopping categories and price ranges. For example, Afterpay focuses on fashion and lifestyle, while Zip Pay covers everything, including larger purchases.

- No Hard Credit Checks Required: These services skip traditional lending checks with just a soft credit check for approval. Unlike personal loans or credit cards, there’s no lengthy application process. Also, most BNPL providers can approve you instantly without affecting your credit score.

- Instant Approval Process: Get approved in seconds for your payment plan, not days like traditional credit. The application process is streamlined through mobile apps or website forms, making it incredibly fast and user-friendly. You just need basic details like your phone number and bank account information.

- Flexible Shopping Options: You’ll find BNPL options both in physical stores via apps and online at checkout. The popularity of these services has led retailers across Australia to adopt them as standard offerings. This widespread acceptance means you can use them at everything from large chains to boutique shops.

The whole process takes about 30 seconds. Throughout this quick setup, you provide basic details, get approved instantly, and your buy now pay later provider handles the rest. Your purchase arrives as normal, but your payment plan stretches the cost across future pay periods.

The Sweet Spot: Why Interest-Free Shopping Wins Hearts

People love interest-free shopping since it allows you to get what you need now without upfront costs or added charges. The appeal goes beyond just splitting payments. It’s about financial flexibility and instant gratification. Here’s the step-by-step experience that hooks millions of Aussies:

Step 1: Choose Your Purchase – You select the item you’ve been wanting but couldn’t justify spending the full amount on today. Our findings show that “Buy now, pay later” makes it suddenly affordable by requiring just 25% upfront.

Step 2: Quick Approval Process – Your later service provider approves you in seconds with a soft credit check. There’s none of the lengthy application process or waiting periods you’d experience with traditional credit options.

Step 3: Enjoy Immediate Satisfaction – Instead of waiting weeks to save the full price, new jackets can be enjoyed right away. This instant gratification without the financial sting makes BNPL addictive for many shoppers.

Step 4: Automated Payment Schedule – Three more payments will automatically be deducted from your bank account every two weeks. The later providers handle all scheduling, so you don’t need to remember payment dates.

Step 5: Zero Extra Costs – When you pay on time, most later providers charge no interest or additional fees. You pay exactly the purchase price, just spread across multiple payments.

Of course, if BNPL were this perfect, everyone would use it without any problems, right?

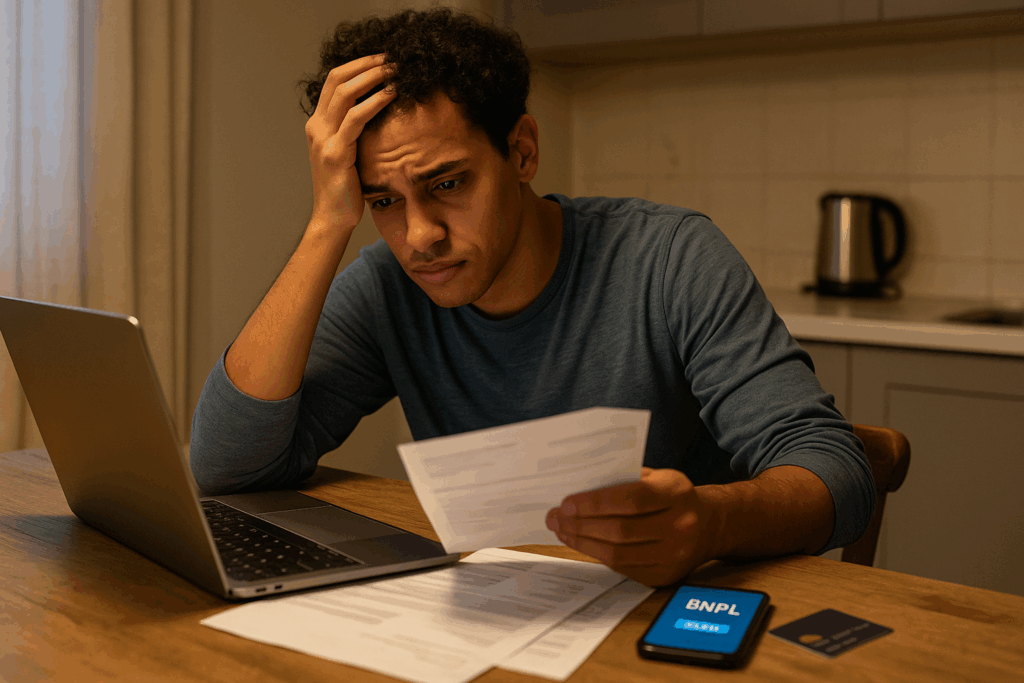

The Flip Side: When Later Payment Gets Costly

The fee-free shopping experience ends when you miss a payment. The consequences are swift: late fees typically hit your account within days, ranging from $10 to $25 per missed payment. Your $100 purchase quickly becomes $125 or more with these additional charges. These late payment fees stack up even faster if you miss multiple payments across different late payment providers.

However, the damage goes beyond just fees. What’s worse, missed payments now appear on credit reports, creating red flags for future lenders. This means banks will see this payment history when you apply for home loans or personal loans later. Unfortunately, many users who struggle with BNPL payments also start missing household bills like rent and utilities, creating a dangerous financial spiral.

Your BNPL Safety Playbook

You can use “buy now, pay later” safely with the right approach and planning. The mindset shift is treating these services like cash, not free money.

Four essential strategies will keep you in control:

Budget for All Payments Upfront

Can you honestly afford four payments over the next six weeks? The answer depends on your current bank balance, upcoming bills, and any unexpected expenses that might pop up. Before clicking buy, take a moment to check these factors carefully. If money feels tight now, it’ll feel tighter when multiple payments start hitting your account automatically.

Limit Yourself to One Provider

Multiple BNPL accounts create payment chaos, and that confusion builds quickly. That’s why it’s better to stick to one later service rather than sign up for several different providers.

When you spread yourself across many overlapping schedules, it makes it hard to track due dates. In turn, spending totals become messy as payments scatter across platforms.

Choose Providers on a Tight Budget

Late payment fees vary dramatically between providers. Some charge $10 for missed payments, while others charge $25 for the same mistake. So compare these fees, spending limits, and payment schedules before signing up with any later service.

Plan Your Emergency Fund Strategy

If you can’t afford the full purchase price today, you probably can’t afford the instalments either. So always keep enough money in your bank account to cover upcoming payments plus unexpected expenses. This simple rule prevents most BNPL financial disasters.

Now that you know how to use BNPL safely, let’s wrap up with some final thoughts on making the right choice for your wallet.

Making Wise Choices That Save Money

Buy now, pay later has revolutionised Australian shopping, but millions face unexpected costs through missed payments and late fees. The solution lies in understanding both the benefits and risks before making your first purchase.

We’ve explored how BNPL works, why people love interest-free shopping, the hidden costs of late payments, and essential safety strategies for responsible usage. Now you have the knowledge to make better financial decisions.

Ready to find genuine deals that protect your wallet? Visit Unsubscribe Deals for curated savings that deliver value without the financial stress.